Legislation Amendment

A new section (19B) has been inserted in the Workers Compensation Act (1987) that now creates an automatic entitlement to compensation should a worker in prescribed employment contract Novel Coronavirus (COVID-19).

The claim liability process is to be treated similar to other claims arising of a gradual nature (disease claims) where employment is considered the main and substantial contributing factor to contraction of the disease.

Prescribed employment is considered to be:

(a) the retail industry (other than businesses providing only on-line retail),

(b) the health care sector, including ambulance officers and public health employees,

(c) disability and aged care facilities,

(d) educational institutions, including pre-schools, schools and tertiary institutions

(other than establishments providing only on-line teaching services),

(e) police and emergency services (including fire brigades and rural fire services),

(f) refuges, halfway houses and homeless shelters,

(g) passenger transport services,

(h) libraries,

(i) courts and tribunals,

(j) correctional centres and detention centres,

(k) restaurants, clubs and hotels,

(l) the construction industry,

(m) places of public entertainment or instruction (including cinemas, museums, galleries, cultural institutions and casinos),

(n) the cleaning industry,

(o) any other type of employment prescribed by the regulations for the purposes of this definition.

The presumption of injury can be rebutted, and as is the case with all frank incident or disease claims, the responsibility is on the employer to establish that the disease was not contracted in the course of employment, or that employment was not the substantial or main contributing factor.

Any claim brought forward by a staff member will need to be reported to your WSIB Account Manager per usual process; at which point we will instruct the insurer to assess liability in accordance with the icare Decision Making Principles.

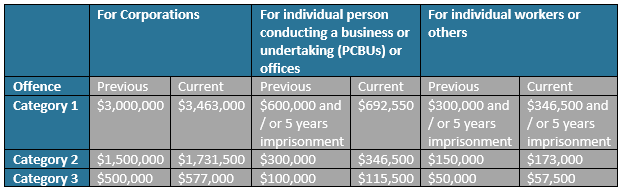

Work Health and Safety

Best Practice Policies and Principles exist which would assist a ‘Prescribed Employer’ in defending any claim brought forward by a member of staff.

Following the NSW Health ‘Industry Guidelines for COVID Safe Workplaces’ will assist employers in maintaining safe premises for staff, contractors and visitors. These guidelines include but not limited to :

– Excluding staff and visitors who are unwell;

– Displaying conditions of entry;

– Limiting entry and exit points to one part of the premises to ensure adherence to maximum capacity restrictions;

– Abiding by social distancing requirements inside the premises (which would include carparks and extensions of the main building);

– Providing adequate resources to maximise hand hygiene;

– Record keeping of all visitors within the premises for a period of no less than 28 days.

Access to the full guidelines can be found here: https://www.nsw.gov.au/covid-19/industry-guidelines

It would also be appropriate to ensure all policies including but not limited to Business Continuity Policy, Infection Prevention & Control Policy, and Pandemic Response Policy is up to date with the appropriate legislation.

Other services exist within the current market which would also assist with providing peace of mind to staff, contractors and visitors. For example, Workplace Cleanliness Inspections and Certification involves an Occupational Hygienist undertaking workplace cleanliness inspections, and can provide an Australian Government recognised clearance certificate.

Finally, a review of the cleaning equipment and routine of cleaning staff or contractors would be appropriate to ensure the virus is not living within the employment premises. Much of the best practice cleaning policy can also be found on the NSW Health Website (link above) and adopted within the place of employment to mitigate risk of COVID infection.

Claims and Premium

Should a Workers Compensation Claim be brought forward by a member of staff, it will be important the employer can demonstrate strict adherence to those Work Health & Safety principles above.

As is the case with all ‘disease claims’; the onus will be on the employer / policy holder to prove the disease or virus has not been contracted through the course of employment, or that employment is not considered the main or substantial contributory factor to onset of the disease / virus.

Should record keeping be maintained, all thorough cleaning schedules and inspection audits be appropriately conducted, and best practice WHS guidelines be strictly observed within the place of business; you will be able to put forward a solid defence for any Workers Compensation Claim be made.

It is important to note COVID related cases not only have the potential for Workers Compensation Claims; but reputational damage that is extremely hard and time consuming to repair. If not for the sake of defending a Workers Compensation Claim; adopting or investing in some of those best practice policies or services will assist in mitigating or avoiding any potential reputational damage inflicted, should a worker or visitor suggest the disease was contracted within your place of employment.

The recent relaxation of restrictions imposed upon the Hospitality Industry (as an example) has been done so with the view of returning life back to normal in a safe and healthy manner. The NSW and Federal Government realise the COVID pandemic has had significant impacts on workers and business owners; and through these principles and relaxing of restrictions they are aiming to take one step closer to ‘normality’.

At the time of writing; the Insurance Regulator (SIRA) were still in talks with all insurers as to how best reduce any COVID related workers compensation claim impacting upon a business. The present consideration is that any COVID-19 claim accepted by a Workers Compensation Insurer is not to be included in the calculation of renewal and adjustment Workers Compensation Premium. This provides some comfort and peace of mind that re-opening business doors may not have adverse affects insofar as a COVID-19 Workers Compensation Claim. It is important to note this stance is subject to change and it is recommended you continue to work closely with your WSIB Account Manager on their interpretation of premium impact.

If you have any questions on this information or any matter, please do not hesitate to reach out to your account manager or the office on (02) 9587 3500 or email us at theteam@wsib.com.au.